The Federal Open Market Committee (FOMC) did what many economists and traders predicted: It cut the benchmark federal funds rate to a lower range of between 4.25% and 4.50%. This follows a 50 basis point cut in September.

“In support of its goals, the Committee decided to lower the target range for the federal funds rate by 1/4 percentage point to 4-1/4 to 4-1/2 percent,” the central bank said in a statement.

“Since earlier in the year, labor market conditions have generally eased, and the unemployment rate has moved up but remains low. Inflation has made progress toward the Committee’s 2 percent objective but remains somewhat elevated.”

But Cleveland Fed President Beth Hammack wasn’t having it. She dissented, pushing to hold rates steady—making her the second official to go against the grain during this streak of reductions.

This adjustment signals a cautious step in navigating the tightrope between controlling inflation and supporting economic growth.

Alongside the rate cut, the Fed also announced a 30-basis-point reduction in the rate paid on its overnight reverse repurchase facility, effectively trimming it by five basis points relative to the federal funds target range.

Derivatives Indicators Show Market Optimism

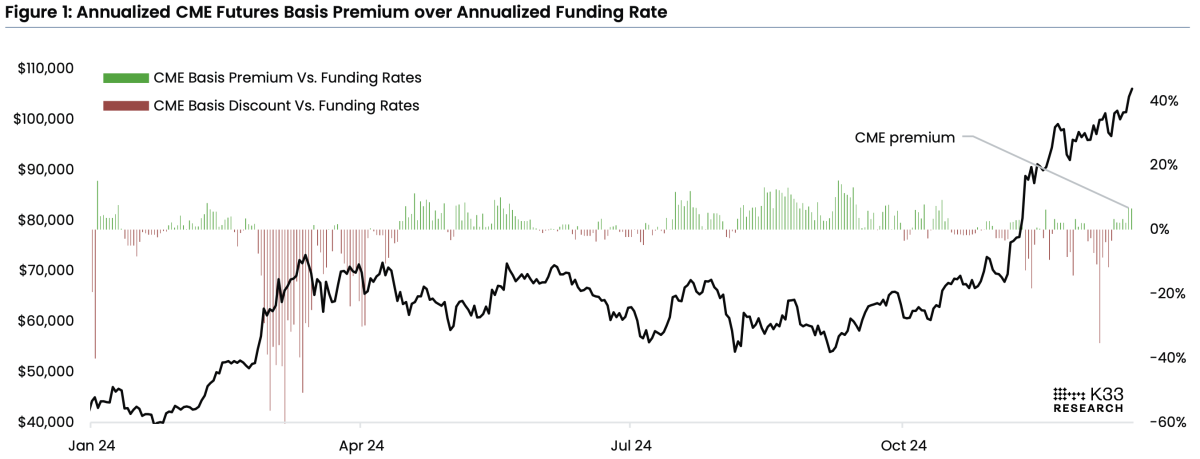

Market indicators suggest growing optimism for bitcoin as CME bitcoin futures open interest surges toward all-time highs, and basis premiums for bitcoin and ether hit 16.4% during the recent breakout, according to a K33 Research report.

Analysts note that contango—where futures prices exceed spot prices—has widened to levels unseen since November 2023.

The December CME bitcoin futures contract is particularly noteworthy, with open interest equivalent to 113,480 BTC, highlighting strong institutional participation.

QCP Capital analysts echoed this sentiment, observing limited bearish signals for bitcoin’s spot price.

However, they noted a cautious tone in the options market, where put options continue to dominate over calls, suggesting traders may still be prioritizing hedging risk rather than chasing the rally aggressively.

“The options market offers a note of caution, with a continued skew toward puts over calls even as spot continue to make new highs—perhaps signaling a preference for hedging rather than aggressively chasing the rally,” QCP Capital analysts said.

QCP Capital analysts cited that a significant regulatory tailwind has also emerged. The US Financial Accounting Standards Board (FASB) recently adopted fair value accounting for bitcoin and other digital assets.

This shift allows companies to recognize fair value gains directly in their net income, making it more attractive for corporate treasuries to hold bitcoin.

“With a supportive regulatory environment driving the recent rally, this could spark a cross-asset feedback loop, where firms holding bitcoin in their treasuries find it easier to raise funds—potentially fueling institutional demand for bitcoin in a non-linear fashion,” QCP Capital analysts said.

Equities Trade Higher After Rate Cut Decision

Major stock indices also spiked higher after the Fed cut interest rates at November’s FOMC meeting. During mid-day trade in the US on Wednesday, the S&P 500 gained 0.59% and the Nasdaq Composite rose 1.33%. However, the Dow dropped 0.015%.

The CBOE Volatility Index (VIX), which measures the expected volatility of the S&P 500 index over the next 30 days, decreased 6% to 15.28 points. Gold increased 0.98% over the past 24 hours to $$2,693.43 per ounce.

Bitcoin traded around $105,317 at publication time, according to data from Tradingview.

The Dot Plot Gets Stingy: Fewer Rate Cuts In 2025

The Fed’s infamous “dot plot” just got a little stingier. The latest projections show officials scaling back their expectations for rate cuts in 2025.

The median forecast now points to only two quarter-point cuts next year, a sharp reduction from the four cuts projected back in September. If you’re counting, that means the benchmark lending rate is expected to drop to 3.9% by the end of 2025, equating to a target range of 3.75% to 4%.

Of the 19 officials involved, 14 predict no more than two cuts in 2025, with five envisioning more aggressive easing—at least 75 basis points worth.

For the longer haul, the committee sees the neutral rate landing at 3%. That’s 0.1 percentage points higher than their last projection, marking a slow but steady drift upward.

Inflation expectations also nudged higher. Headline inflation is now expected to hit 2.4% in 2025, up from the 2.3% forecast in September.

Core inflation isn’t looking much better, climbing from 2.6% to 2.8%. Despite the Fed’s relentless efforts, their dream of a 2% inflation target remains, well, just that—a dream.

The economy isn’t escaping unscathed either. Projections for GDP growth were bumped up to 2.5% for the year, a half-percentage-point jump from September’s estimates. But the long-term forecast isn’t so rosy, with growth expected to crawl back to the Fed’s usual 1.8% projection after 2025.

Mortgage Rates Stay Stubborn

If you’re hoping that rate cuts mean cheaper mortgages, think again. The average 30-year fixed mortgage rate ticked up to 6.75% last week from 6.67% the week before, according to the Mortgage Bankers Association. Turns out, Treasury yields and broader economic pressures have more say here than the Fed’s tweaks.

“Mortgage rates have gone up—not down—since the Fed started cutting interest rates in September,” said Greg McBride, chief financial analyst at Bankrate. With long-term bond yields surging thanks to fewer anticipated rate cuts in 2025, mortgage rates remain pinned close to 7%.

For homeowners with fixed-rate mortgages, this means no immediate changes—unless they refinance or sell and jump into a new loan. But buyers looking to lock in a 30-year mortgage might catch a tiny break.

A $350,000 loan at 6.6% would cost $56 less per month compared to November’s 6.84% peak. Over 30 years, that’s a savings of $20,160, according to LendingTree senior economic analyst Jacob Channel. Not exactly game-changing, but every penny counts when rates are this high.

Student Loans And Savings Accounts: Mixed Bag

Federal student loan borrowers won’t feel a thing from these cuts. Those rates are fixed, locked in at disbursement, and untouched by the Fed’s moves.

Private student loans, however, are a different story. Variable-rate loans tied to benchmarks like the Treasury bill will eventually fall, shaving a few bucks off monthly payments.

Mark Kantrowitz, a higher education finance expert, estimates that a 25-basis-point rate cut would reduce monthly payments on a 10-year private student loan by just $1 to $1.25. Not much to write home about.

Refinancing into fixed-rate private loans could help borrowers save more down the line, but it’s a gamble. You’d be trading federal loan protections—like income-driven repayment and forgiveness programs—for a lower rate. That’s a tough call in this economy.

For savers, the picture’s a bit brighter. Online savings accounts and certificates of deposit (CDs) continue to flaunt competitive rates, thanks to the Fed’s earlier rate hikes.

Top-yielding savings accounts are still paying up to 5% annual percentage yield (APY), a figure not seen in nearly 20 years. CDs aren’t far behind, with some one-year terms offering over 4.5%.

McBride says these slower rate cuts are good news for savers. “The most competitive yields on savings accounts and CDs still outpace inflation,” he noted. Translation? If you’re parking cash, you’re winning. If you’re borrowing, not so much.

The Balancing Act Continues

The Fed’s statement wasn’t all about cuts. It also reiterated that the risks to achieving inflation and employment goals are “roughly in balance.”

The committee emphasized its data-driven approach, vowing to assess incoming numbers and evolving risks before making further moves.

For now, the Fed’s cautious tone signals a wait-and-see approach. Whether more cuts are on the horizon depends on how the economy shapes up in the coming months. But one thing’s clear: This isn’t a free pass to assume rates will plummet anytime soon.